Investors discuss myths and misconceptions that derail early conversations, share signals of fundraising readiness and highlight region specific dynamics that affect the fundraising process.

Reality: Equity comes at a higher cost for investors, so VC is an expensive source of capital that demands rapid growth, repeated fundraising, and a clear path to exit.

Reality: In Africa, investors are rarely betting on ideas, they’re betting on evidence of execution.

Reality: Execution follows validating real customer pain points, not just building technology in isolation.

At the pre-seed stage, the bar is often less about perfect traction or polished numbers, and more about whether a founder demonstrates clarity, credibility, and momentum.

From Cairo to Cape Town, Lagos to Nairobi, regional ecosystems carry distinct histories, capital flows, and cultural norms that influence how founders are perceived and how businesses are benchmarked.

From Cairo to Cape Town, Lagos to Nairobi, regional ecosystems carry distinct histories, capital flows, and cultural norms that influence how founders are perceived and how businesses are benchmarked.

“If your business is focused on helping people buy or sell, it’s important to consider whether the market and model allow for true venture-scale growth. Technology should meaningfully expand efficiency and reach — not just digitize existing limitations — so that the opportunity is large enough, the solution is highly scalable, and the economics remain strong as you grow.”

Jasiel K.N. Martin-Odoom

Accion Ventures

“You give someone a million dollars, and very often that scrappy mindset goes right out the window. But the capital-efficient founders? They’re using Excel sheets, still calling customers on WhatsApp, and leveraging USSD where required instead of apps. They understand that outcomes are more important than fancy outlooks.”

Christine Namara

F6 Ventures

“Fundraising can sometimes give you a feeling of false productivity. If you’re doing it the wrong way, at the wrong time, it’s just a big time suck.”

Ambar van der Wath

Baobab Network

“Most companies are not going to be venture-backable — and that’s not necessarily a bad thing. Venture funds are targeting returns north of 3x, and they’re doing it in hard currency, which makes it especially difficult for startups operating in volatile markets.”

Peter Wamburu

Vested World

Provide the following information to get access

Provide the following information to get access

A fundamental misconception many early-stage founders in Africa have is that they see venture capital as growth fuel without recognising its deeper obligations. Some founders believe they can keep raising indefinitely while holding on to their businesses, without any real sense of what an exit might look like. The reality is that VC money is rarely patient, and it is structured around a cycle of fundraising, dilution, and ultimately, delivering returns through an exit.

This knowledge gap creates a dangerous misalignment between founder intentions and investor expectations. This lack of shared clarity not only frustrates relationships between founders and investors, but also hampers the healthy development of venture-backed businesses in Africa.

Raising venture capital is not just about accessing money. It is about entering into a binding relationship that comes with growth targets, ownership trade-offs, and an eventual exit. Failing to recognise this from the start can make fundraising itself harder, as investors can quickly spot when a founder’s long-term vision is misaligned with the realities of venture capital from how they talk about growth dynamics.

Many founders assume that the natural sequence of building a startup is to raise capital first and validate their ideas later. The logic feels persuasive: if investors believe in the idea, the money will follow, and the product can finally get built. But this mindset often traps founders in endless pitching cycles before they’ve proven anything real about their product, market, or ability to execute.

What investors are scanning for at the pre-seed stage is not a perfect pitch deck or financial model, but evidence that the founder can create momentum with limited resources. Founders who spend most of their energy on pitching without validation risk burning time, goodwill, and credibility. What sets successful pre-seed founders apart is their ability to push forward with limited resources, showing that they can learn, iterate, and gain early market buy-in before outside capital comes in. This could be proven by a scrappy but functional product, a pilot customer, a partnership, or even a tested hypothesis that demonstrates progress.

Investors back proof, not promises. Founders who prioritize validation build stronger relationships, signal resilience, and unlock capital on more favorable terms.

Many early-stage founders fall into the trap of obsessing over product development, from polishing features to refining technology, and building in isolation before ever validating whether customers actually want what they are building. The assumption is that a brilliant product will naturally attract users. In reality, what investors want to see, even at pre-seed, is that a founder deeply understands their customer’s pain points and has tested solutions that address them.

Investors across the continent guard against “over-engineering” at pre-seed, emphasizing that the real mark of readiness is not a flashy MVP but customer insights. Founders who spend their early days speaking directly with potential users, testing hypotheses, and iterating based on feedback are better positioned to raise. They can show evidence that their product is not only functional but relevant, tackling a pain point customers recognise and are willing to pay for.

Traction does not come from a beautiful product, but from proof that it solves a customer’s real problem. In early-stage African markets, execution means grounding your business in customer validation before scaling your technology.

Many founders at the pre-seed stage believe that negotiating the highest possible valuation is a signal of strength. A bigger number seems to validate the idea, boost credibility in the ecosystem, and protect against dilution. But in practice, inflated early valuations often create more harm than good.

A high valuation does not guarantee long-term success, it raises the bar for growth and traction at every subsequent round. If the company can not keep up with its projections, the founder risks a down round: raising capital at a lower valuation than before. Down rounds not only dilute ownership further but also damage perception, shaking investor confidence and team morale.What’s more, investors are not always impressed by inflated valuations. In fact, they can be put off by them. Experienced pre-seed and seed investors look for a balanced approach: a valuation that reflects the risk and stage of the company, while leaving room for future growth and follow-on funding. An unrealistic number can close doors instead of opening them.

For African founders especially, where fundraising cycles are long and capital is more concentrated, playing the long game matters. A valuation that is “good enough” to raise what you need while protecting ownership and signaling discipline is more valuable than a flashy headline figure that sets you up for painful corrections down the line.

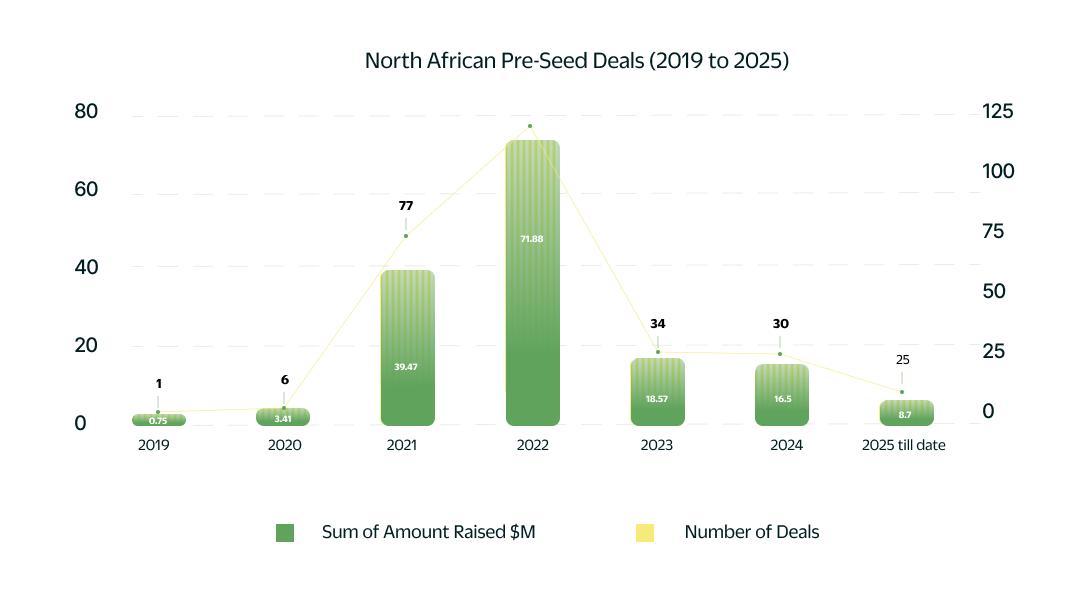

Northern Africa has emerged as one of the most active regions for pre-seed fundraising on the continent. Between 2019 and 2025, startups in the region closed 293 pre-seed rounds, raising a combined $159.3M. Egypt is the clear anchor, contributing nearly two-thirds of all deals and over 80% of capital, but Morocco, Tunisia, and a nascent Algeria are steadily building momentum, offering investors fresh entry points into underexplored markets.

What makes Northern Africa distinct is not just its numbers but the character of its pipeline. This reflects the region’s engineering talent base and its proximity to European and MENA ecosystems.North African founders face a unique set of expectations shaped by geography. Global investors see them through a Middle Eastern lens, while pan-African investors often exclude the region citing cultural and operational differences.

Investors also assume North African ecosystems are more developed than they actually are, so they come with higher expectations around governance, financial reporting, or scalability. Founders in the region often end up needing to over-explain both the opportunities and the challenges of building in North Africa. This dual identity raises the bar for founders, who must prove they can scale both across the continent and beyond it.

This tension also plays out in expansion strategies. Investors observe that many founders look northward to the GCC, hoping to scale into Saudi or Dubai. But products built for lower-income African contexts often struggle in Gulf markets, where customer needs differ. Expansion southward into Africa may make more strategic sense, but the allure of GCC capital and prestige is strong.

Even storytelling is shaped by this duality. Decks are polished, TAMs are inflated, and founders adopt the Silicon Valley style pitch favored by Gulf investors. Yet founders are also navigating very real on-the-ground realities such as fragmented markets, currency fluctuations, and regulatory hurdles. This dual pressure means North African founders must be exceptionally versatile: capable of delivering sleek, global-ready storytelling while also grounding their businesses in the realities of local execution.

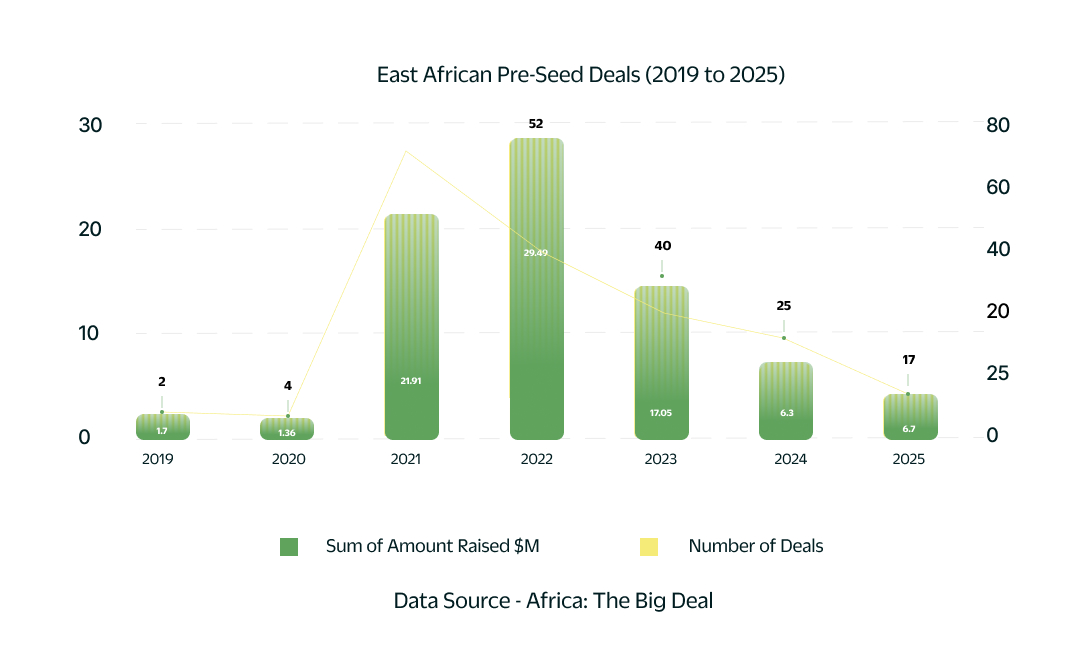

Between 2019 and 2025, startups in the region closed 204 pre-seed rounds worth an estimated $81.4M. The cycle peaked in 2021–2022, when activity surged to more than 120 deals worth $51.4M following the general boom, before declining sharply to just $3.8M across 10 deals in 2025 till date. Kenya dominates, accounting for over two-thirds of deals and capital, but Uganda, Rwanda, Ethiopia, and Tanzania have started picking up pace, with Tanzania in particular showing new momentum in 2025.

Investors with cross-regional mandates emphasize that the yardstick is broadly consistent. This universality means East African founders must meet the same performance benchmarks as peers in Lagos or Cairo, even when operating in smaller or more fragmented markets.

However, what does differ is the style and conviction with which East African founders sell their businesses. West African founders are often more extroverted and aggressive in their pitch delivery, while East African founders tend to “let their business do the talking.” In practice, this humility can undersell otherwise solid fundamentals. For East African founders, the takeaway is clear: strong numbers must be matched with equally strong storytelling.

The overlooked strength, however, is structural. The East African Community (EAC) is one of the most integrated economic blocs on the continent, offering a combined market of more than 300 million people. Yet this strength is often underplayed in fundraising conversations. Instead of framing traction market by market, founders could emphasise their capacity to scale seamlessly across borders, positioning themselves as regional players from the outset. In doing so, East African startups would not only match the confidence of their peers in Lagos or Cairo, but also unlock the full value of a region uniquely built for cross-border growth.

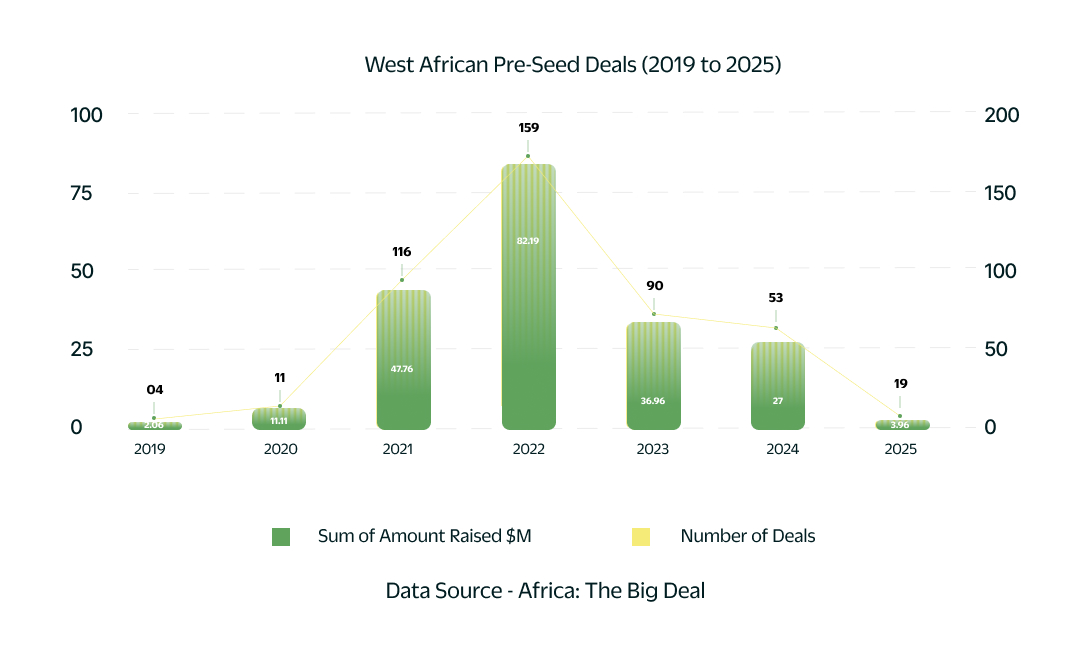

West Africa saw 452 pre-seed deals worth an estimated $211M between 2019 and 2025, making it the single largest sub-region for early capital on the continent. On the surface, this positions West Africa as the engine of Africa’s startup pipeline, but a data drill reveals a more nuanced reality. Deal sizes are highly skewed, and capital is unevenly distributed across countries and sectors.

Founders in Francophone West Africa are adapting models that have succeeded in East and Anglophone West Africa. This dynamic matters because it lowers the risk profile of early bets as investors can recognize business models that have already been validated elsewhere, while founders localize them for their markets.

Francophone West African founders often stand out for their European orientation, a reflection of educational and professional ties to France and continental Europe. This European alignment is reinforced by a strong pipeline of engineering talent, with founders described as “incredibly technically competent” thanks to the region’s longstanding academic traditions. The result is an ecosystem that blends strong technical foundations with a cross-border perspective, giving it a distinct identity within Africa’s early-stage landscape.

Yet, this European orientation also introduces complexities. Many startups end up being domiciled in France or in Mauritius and that adds a layer of complication to any kind of regular investor that’s either US-based or Anglophone Africa based. These structures can make deals more cumbersome for international investors unfamiliar with Francophone legal and financial ecosystems. Still, founders themselves bring a refreshing humility and pragmatism to fundraising conversations, a sharp contrast to what investors often encounter in Lagos.

Beyond behavioural dynamics, Francophone West African founders also possess structural and linguistic advantages. A shared currency, similar regulatory environments, and cultural ties make Francophone West Africa more integrated than it might appear from the outside. While no single country rivals Nigeria in domestic market size, founders who scale across Dakar, Abidjan, and Lomé can quickly reach meaningful regional traction. Additionally, founders can benefit from the linguistic flexibility once they overcome the language barrier.

As Francophone West African founders are marked by pragmatism, Anglophone West African founders, particularly Nigeria and Ghana, are defined by their ambition. This ambitious mindset is reflected not only in how they set valuations but also in how they position their companies for scale. This culture of “thinking big” is reinforced by the macroeconomic context in the region. Frequent bouts of currency depreciation in Nigeria and Ghana force founders to look beyond their domestic markets to protect and grow value. In practice, this means investors tend to demand stronger traction metrics and more proof of resilience from them than they might expect elsewhere.Diaspora proximity further shapes the fundraising landscape. While Lagos-based founders are not necessarily perceived differently, diaspora founders often benefit from direct access to capital networks in Europe and North America. As many large funds are domiciled outside of the continent, then there is significant advantage if the founder can meet funders where they are. This advantage helps explain why diaspora-led teams are often among the most visible in large fundraising rounds, even as locally based founders carry the weight of navigating operational complexity on the ground.

Southern Africa’s pre-seed ecosystem has raised $43.4M across 110 deals since 2019, making it the region with the least deals (in volume and value) on the continent across the years. In 2025 however, South Africa recorded the second-highest capital raised on the continent at $8.6M, behind only North Africa, despite closing just 11 deals. This suggests that average cheque sizes in the region are higher than in most other regions.

South Africa anchors Southern Africa’s pre-seed landscape, accounting for the overwhelming majority of deals and capital raised in the region. Between 2019 and 2025, South African startups closed over 90 pre-seed rounds totaling most of the $43M raised across the region. Over 80% of both deals and dollars are concentrated there, with only light activity seen in Zimbabwe, Zambia, Mozambique, Namibia, and Angola. Deal activity peaked in 2021–2022 with over 30 rounds each year, but has slowed since then in line with the broader funding downturn.

South Africa benefits from strong local capital bases that can sustain founders through the earliest stages. Unlike in Nigeria or Kenya, where many founders must raise externally to even begin, South African founders often bootstrap using friends-and-family networks supported by the country’s higher GDP per capita. This dynamic helps explain why cheque sizes are larger and deal counts fewer. The depth of domestic capital allows startups to grow further before seeking institutional funding, meaning fewer but more substantial rounds when they do enter the venture pipeline.

At the same time, South Africa’s relative isolation makes scaling beyond its borders more challenging, which may limit the number of companies positioned for VC-style growth. The relative maturity of the South African economy also contributes to this inward-looking dynamic. With a wealthier consumer base, a diversified economy, and deeper pools of capital across asset classes, founders can build meaningful businesses without needing to expand regionally or rely on early-stage venture funding. This same maturity can dampen the type of rapid, aggressive scaling that characterizes venture-backed ecosystems elsewhere on the continent. Nigerian and Kenyan founders, lacking similar domestic safety nets, are often compelled to raise external capital earlier and think regionally from the start. By contrast, many South African startups are content to serve their local market, which is relatively large and sophisticated by African standards.